People across NSW are taking advantage of a lifelong investment opportunity that can offer them a return on investment of 15% – 18%. Granny Flats are an opportunity for investors to ‘make money from their own backyard’.

When it comes to financing your new granny flat, you should speak with your current lender or one of our Broker Lending Partners. They will be able to give you advice and recommendations on how to structure any finance sought.

In most cases you can use the current equity available on the property as the security. For this reason, 100% finance is often available, as the overall loan-to-value-ratio (LVR) is acceptable to the lender.

The construction of a granny flat also provides you with an opportunity to review any current home loan you have and refinance to a cheaper lender, while obtaining the required loan increase.

Gaining finance for two dwellings on one title is generally viewed by lenders in a similar light to a typical home loan.

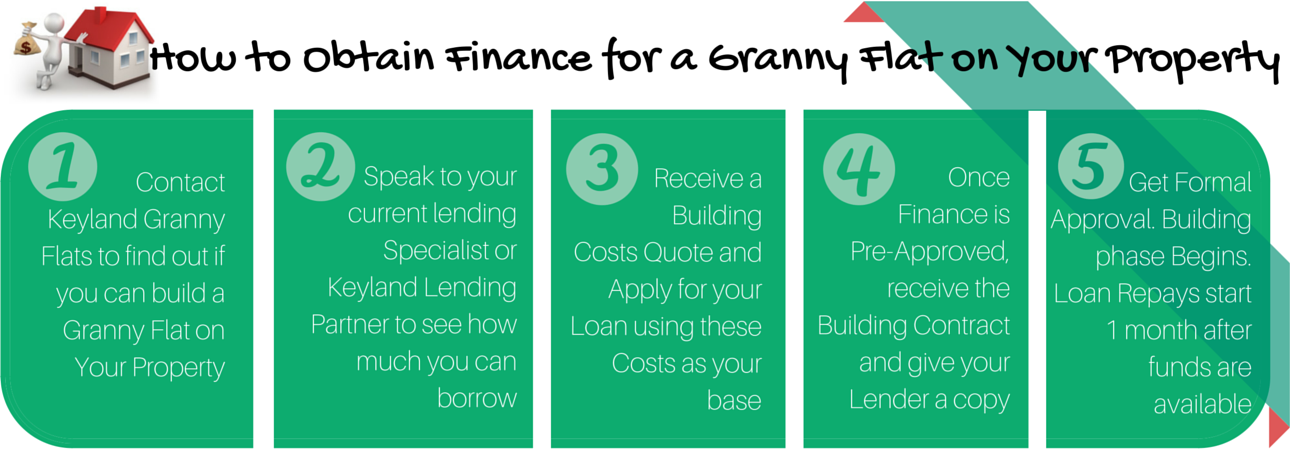

- 1. Speak to a Qualified Lending Specialist to find out how much you can borrow against your Current Home Equity

- 2. Receive a Complete Building Quote from Keyland showing the full price of constructing your Granny Flat. Apply for Finance Pre-Approval based on these costs

- 3. Once pre-approved you are able to sign the completed Building Contracts with Keyland. Our Lending Team send the Building Contracts and any other outstanding items to your lender, making the whole process easy for you.

- 4. Within a few days your Loan can be Fully Approved

- 5. After Loan Approval, the Building Phase will be completed. Loan repayments begin 1 month after funds being made available to you. The Keys to your Keyland Granny Flat are handed over upon completion (12 weeks).

The banks will lend based on the lesser of the ‘on-completion’ value of the house and granny flat, or the current value of your property plus the cost of building the granny flat.

To keep your loan application simple, the Keyland Strategy is to provide you with all your costs upfront. This enables you to keep your loan application simple by including all of your costs in the building contract rather than as separate quotes. This saves the lender time and effort.

The best way to go about this is to gain pre-approval once you’ve decided to carry out the project, and only going for formal approval once you’ve collated the final building contract and plans.

Keyland Lending Partners Include